Despite slight declines in tender rejection rates since peaking in February, the truckload market appears to be entering a prolonged transitional phase. As fuel prices surge, dry van spot rates are rising again, indicating that the market is becoming increasingly tight. This trend suggests that the truckload market may struggle to recover from its current state of disruption, with potential long-term consequences for shippers and carriers alike.

Understanding tender rejections is crucial in interpreting the truckload market. While spot rates tend to correlate with rejection rates over time, they are heavily influenced by sentiment and the transactional (spot) market, which accounts for roughly 15–30% of total volume. The lack of price discovery in tender rejections makes them a more objective signal, reflecting operational decisions rather than market sentiment.

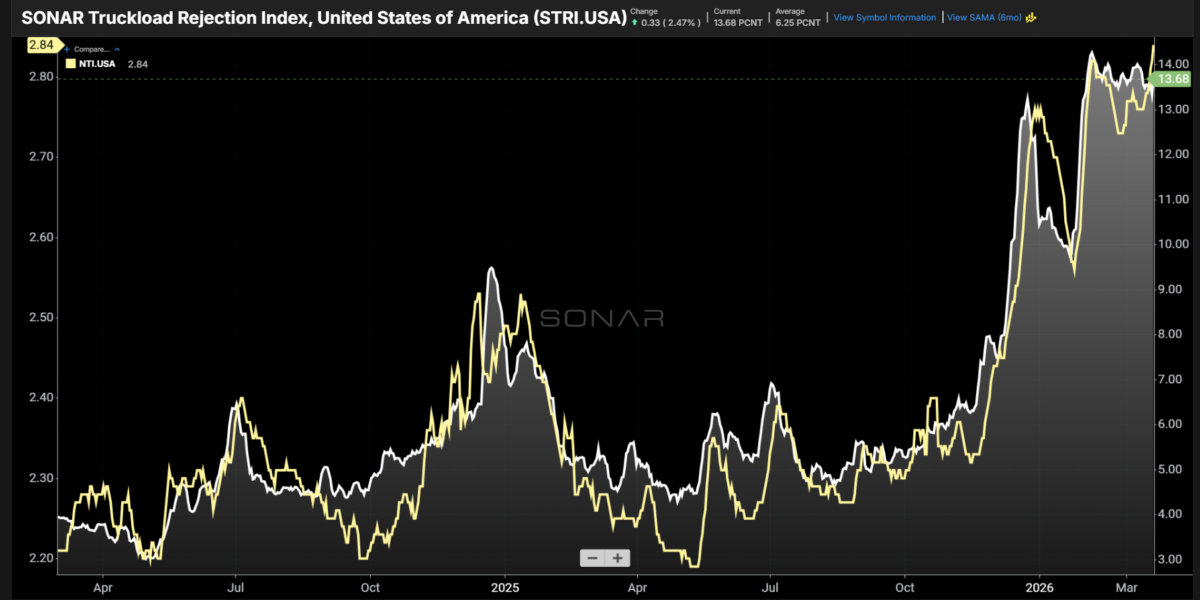

The SONAR Truckload Rejection Index (STRI) peaked at 14.27% on February 5 and has only fallen to 13.35% as of March 18. This decline is modest compared to previous periods, suggesting that the market may be experiencing a prolonged tightening rather than a short-term disruption.

Last year's rejection rates peaked at 7.81% on January 15 following several winter storms across the southern and central U.S., before returning to trend by early February. In contrast, this year's STRI pattern resembles the elevated, prolonged tightening seen in 2021 during the pandemic—albeit at a lower level.

The current market environment lacks the strong demand that defined 2021, which was heavily driven by import volumes and port activity. Instead, shippers are increasingly shifting long-haul freight back to intermodal, indicating a shift towards more efficient transportation options.

Data on the full impact of factors such as ELP enforcement, non-domiciled CDLs, ELD compliance, and questionable CDL issuance is limited. However, industry estimates suggest that these regulatory pressures could amount to several hundred thousand drivers over time, further exacerbating the truckload capacity shortage.

The recent rise in spot and rejection rates has occurred with minimal seasonal support so far. Produce season is approaching and has the potential to significantly disrupt transportation markets. Even with limited volumes, rates have already begun to edge higher.

Roadcheck Week has also become a major annual disruptor, often pulling rejection rates out of their lows. As the truckload market enters this prolonged transitional period, shippers and carriers must be prepared for continued volatility and potential long-term consequences.

The truckload market's current state of disruption highlights the need for greater transparency and cooperation between shippers, carriers, and regulatory bodies. By working together to address capacity shortages and regulatory pressures, the industry can mitigate the impact of these disruptions and promote a more stable transportation market.

The truckload market may be entering an early stage of a prolonged transitional period, with additional disruption likely from seasonal factors and new regulatory pressures.