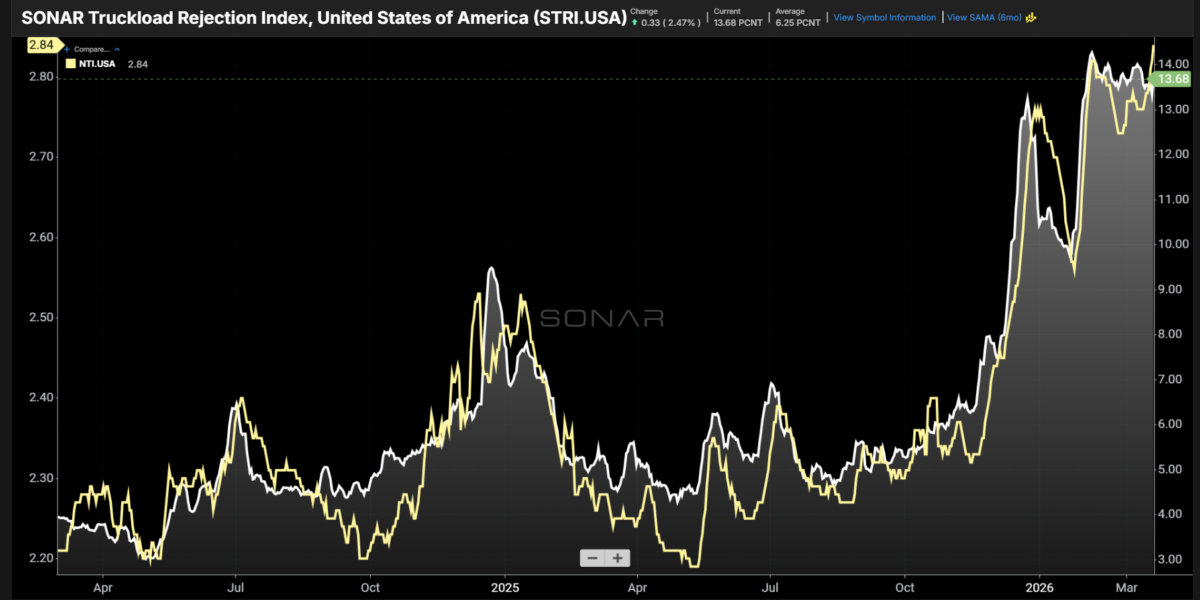

National dry van spot rates have broken out to a new cycle high of $2.89 per mile, according to the SONAR National Truckload Index (NTI.USA), marking the strongest level since 2022. This significant increase reflects the market's shift toward carriers gaining pricing power and underscores accelerating tightness in the industry. The recent weekly gain of $0.12 per mile further emphasizes the need for shippers to be prepared for potential rate increases.

The trucking capacity market has seen a sharp rise in rates, with spot rates recapturing roughly $0.50-$0.60 per mile net of fuel over recent months. This represents a 20-25% year-over-year recovery in key lanes and metrics, with volumes holding at multi-year highs reminiscent of late 2022. The return of industrial demand remains the core engine driving this trend.

The decline in trucking capacity due to multi-year carrier attrition has left the market highly responsive to any demand pickup. National tender rejection rates sit stubbornly in the low-to-mid teens, with the Midwest leading above 18% and tightness now spreading more broadly. This suggests that shippers will face increased competition for available trucks.

The recent surge in trucking capacity tightening is also driven by seasonal layers, including the West Coast awakening. The delayed but powerful post-CNY import surge has created synchronized tightness across the industry. As long-haul carriers chase West-to-East port loads for their superior length of haul, interior markets face no relief and expect even tighter conditions.

The Midwest's industrial strength and elevated rejections mean any capacity drain will intensify pressure, not ease it. This creates a classic 'magnet' for capacity, with trucks repositioning westward from Midwest/Southeast corridors to capture higher-paying outbound freight. As a result, shippers can expect even tighter conditions back east.

The recent surge in trucking rates and capacity tightening highlights the need for shippers to plan ahead and adapt to changing market conditions. With volumes holding at multi-year highs and industrial demand driving the trend, shippers must be prepared to negotiate with carriers and manage their supply chains effectively.

Broader indicators align to support this trend, including a surge in inbound containers and outbound tenders recovering. As the industry awakens from its post-CNY slowdown, shippers can expect even tighter conditions and increased competition for available trucks.

The recent increase in trucking rates and capacity tightening is a clear indication that the industry is shifting toward carriers gaining pricing power. Shippers must be prepared to adapt to this new reality and negotiate with carriers to secure favorable terms.

As the market continues to tighten, shippers can expect to see even tighter conditions and increased competition for available trucks. With industrial demand driving the trend and capacity tightening on the rise, it is essential for shippers to plan ahead and manage their supply chains effectively.

The recent surge in trucking rates and capacity tightening highlights the need for shippers to plan ahead and adapt to changing market conditions.