Shippers are facing a new reality in 2026 as costs continue to rise despite lagging volumes. The latest quarterly U.S. Bank Freight Payment Index – Rates Edition reveals a freight market where carriers are gaining pricing power through capacity discipline rather than increased demand. This trend is expected to have far-reaching implications for shippers and carriers alike.

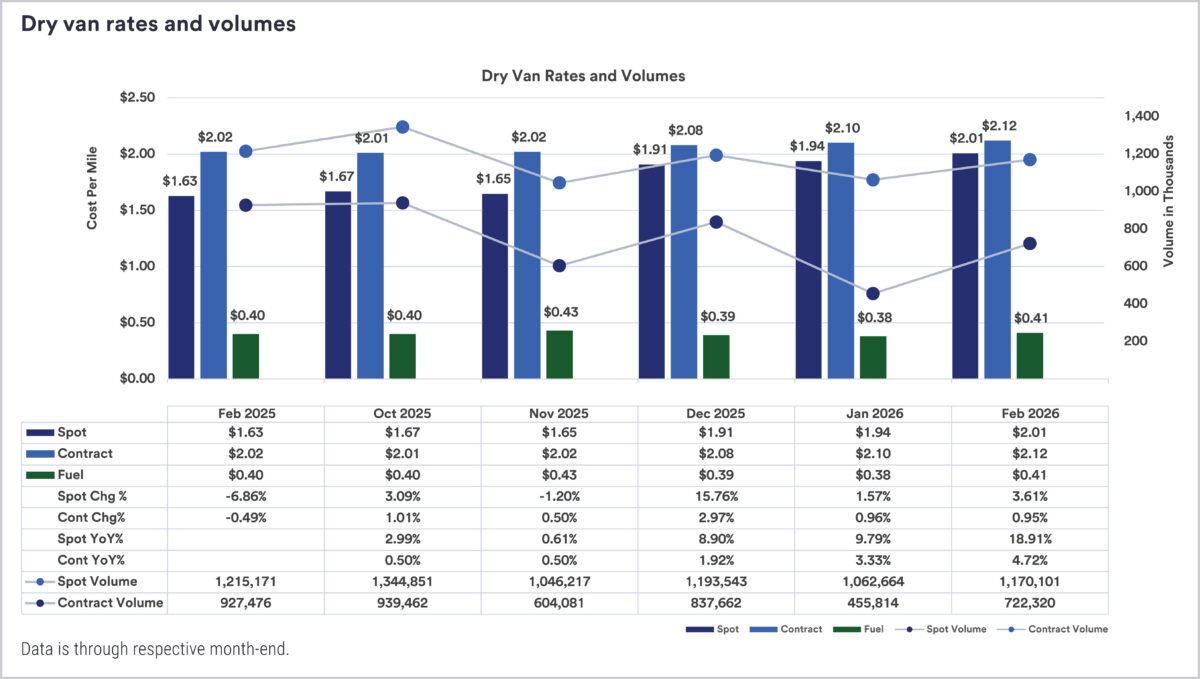

Spot rates rebounded in February, reaching $2.01 per mile after falling to $1.65 in November 2025. Contract rates also ticked up, increasing to $2.12 per mile from $1.99 over the same period. This marks a fourth consecutive month of increases across both pricing mechanisms.

The spot market has shown significant improvement, with spot linehaul climbing roughly 28 percent through February 2026. In contrast, contract pricing has remained relatively stable, rising only about 6.5 percent from $1.99 to $2.12 per mile over the same period.

The inflection point in the freight market occurred in December 2025, with spot linehaul jumping from $1.65 to $1.91 per mile. This coincided with a 15.76 percent month-over-month increase in spot activity and a 14 percent rise in spot volume.

The rapid compression of the gap between contract and spot rates is another key development. A year ago, the contract premium stood at about $0.39 per mile, but by March 2026, it had narrowed to roughly $0.11 – a compression of approximately $0.28.

This narrowing suggests that spot rates are catching up to contract levels, reducing the cushion shippers rely on when balancing tender acceptance and routing decisions. As a result, carriers will need to be more selective about the freight they accept in order to maintain their pricing power.

The year-over-year data highlights just how unusual this setup is. Spot linehaul increased by 23.3 percent while contract linehaul rose only 5 percent from March 2025 through February 2026. Meanwhile, spot volume fell approximately 3.7 percent and contract volume dropped about 22.1 percent.

The divergence between pricing and activity is a significant indicator of the market's behavior. Pricing strengthened even as activity remained under pressure, suggesting that capacity is being managed more tightly than demand is growing. This appears consistent with a supply-led shift where carriers protect yield and become more selective about the freight they accept.

As shippers navigate this new reality, they will need to carefully consider their budget constraints and routing options in order to stay competitive. The shift in pricing power from demand to capacity discipline is a significant development in the freight market, and it will be interesting to see how carriers respond to this trend.

The shift in pricing power from demand to capacity discipline is a significant development in the freight market.